Are you searching for the best mortgage rates today? If you're planning to buy a home or refinance your current mortgage, understanding today's mortgage rates is crucial for making informed financial decisions. Mortgage rates fluctuate daily, influenced by various economic factors, and staying updated with the latest rates can significantly impact your long-term financial health.

Whether you're a first-time homebuyer or a seasoned property owner, knowing how mortgage rates work and what drives them can help you save thousands of dollars over the life of your loan. In this comprehensive guide, we'll explore everything you need to know about mortgage rates today, including how they're determined, the factors that affect them, and strategies to secure the best rates available.

By the end of this article, you'll have a clear understanding of mortgage rates, empowering you to make smarter choices when purchasing or refinancing a home. Let's dive in!

Read also:Chloe Guidry Rising Star In The Entertainment World

Table of Contents

- Current Mortgage Rates Today

- Factors Affecting Mortgage Rates

- Types of Mortgage Loans

- Fixed vs. Variable Mortgage Rates

- How Your Credit Score Impacts Mortgage Rates

- The Role of Down Payment in Mortgage Rates

- Economic Indicators and Mortgage Rates

- Tips for Securing the Best Mortgage Rates Today

- Refinancing Options and Mortgage Rates

- Future Predictions for Mortgage Rates

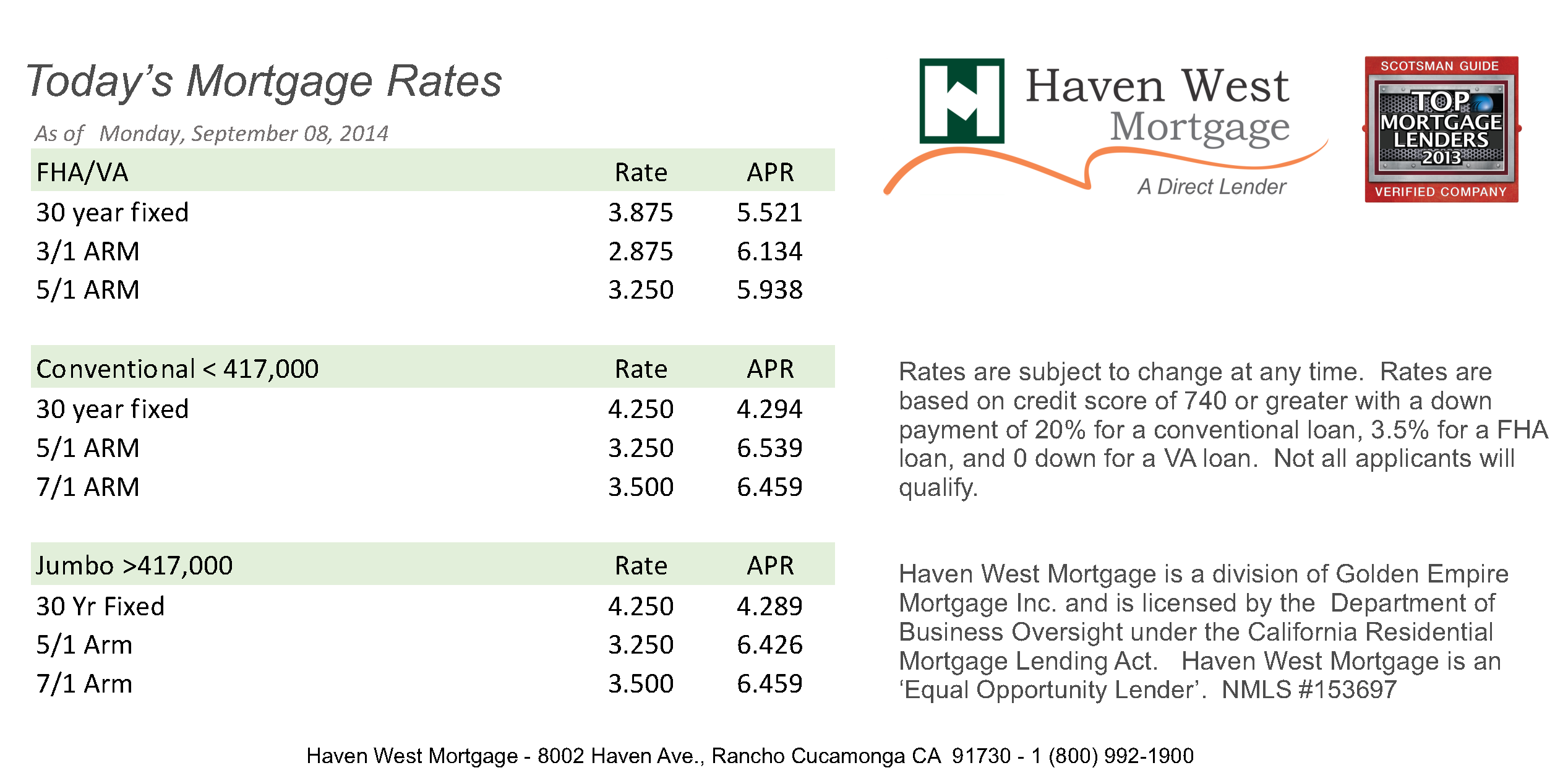

Current Mortgage Rates Today

Mortgage rates today are influenced by a complex mix of economic factors, including inflation, Federal Reserve policies, and the overall health of the housing market. As of the latest data, 30-year fixed mortgage rates average around 6.5%, while 15-year fixed rates hover slightly lower at approximately 5.8%. Adjustable-rate mortgages (ARMs) often offer lower initial rates, making them an attractive option for borrowers planning to sell or refinance within a few years.

It's important to note that these rates are subject to change daily. Borrowers should regularly monitor rate fluctuations and consult with a trusted lender to secure the most favorable terms. Additionally, regional differences can impact rates, so it's essential to compare offers from multiple lenders in your area.

Why Are Mortgage Rates Important?

- Mortgage rates directly affect your monthly payments and the total cost of your loan.

- Lower rates can result in significant savings over the life of the mortgage.

- Understanding rates helps you make informed decisions about buying or refinancing.

Factors Affecting Mortgage Rates

Mortgage rates are not set arbitrarily; they are influenced by several key factors. These include the Federal Reserve's monetary policies, inflation rates, bond market performance, and supply and demand dynamics within the housing market. Additionally, individual borrower characteristics, such as credit score and debt-to-income ratio, play a significant role in determining the rates offered by lenders.

Economic indicators like unemployment rates and Gross Domestic Product (GDP) growth also impact mortgage rates. When the economy is strong, rates tend to rise as lenders anticipate higher inflation. Conversely, during economic downturns, rates may decrease to stimulate borrowing and spending.

Key Economic Factors

- Federal Reserve Policies: The central bank's decisions on interest rates influence mortgage rates.

- Inflation: Rising inflation typically leads to higher mortgage rates.

- Bond Market Performance: Mortgage rates often move in tandem with the yields on 10-year Treasury bonds.

Types of Mortgage Loans

There are various types of mortgage loans available, each with its own set of features and benefits. The most common types include conventional loans, Federal Housing Administration (FHA) loans, Veterans Affairs (VA) loans, and United States Department of Agriculture (USDA) loans. Each type caters to different borrower profiles and financial situations.

Conventional loans are ideal for borrowers with strong credit scores and substantial down payments. FHA loans, on the other hand, are designed for first-time homebuyers or those with lower credit scores. VA loans offer favorable terms to eligible veterans and active-duty service members, while USDA loans are available to rural property buyers.

Read also:Tyler Lepley A Rising Star In The World Of Entertainment

Popular Mortgage Types

- Conventional Loans

- FHA Loans

- VA Loans

- USDA Loans

Fixed vs. Variable Mortgage Rates

Choosing between fixed and variable mortgage rates is one of the most important decisions a borrower can make. Fixed-rate mortgages offer stability, with the interest rate remaining constant throughout the loan term. This makes budgeting easier and protects borrowers from rate increases. However, fixed rates are often higher than initial variable rates.

Variable-rate mortgages, also known as adjustable-rate mortgages (ARMs), offer lower initial rates but come with the risk of rate increases over time. These loans are best suited for borrowers who plan to sell or refinance their homes before the rate adjustment period begins.

Pros and Cons of Fixed vs. Variable Rates

- Fixed Rates: Predictable payments, protection from rate hikes.

- Variable Rates: Lower initial rates, potential savings if rates decrease.

How Your Credit Score Impacts Mortgage Rates

Your credit score is one of the most significant factors influencing the mortgage rates you're offered. Lenders view borrowers with higher credit scores as lower-risk, resulting in more favorable rates. Conversely, lower credit scores may lead to higher rates or even loan denial.

To secure the best mortgage rates today, it's essential to maintain a healthy credit score. This involves paying bills on time, keeping credit utilization low, and addressing any errors on your credit report.

Improving Your Credit Score

- Pay bills on time.

- Reduce credit card balances.

- Monitor credit reports for errors.

The Role of Down Payment in Mortgage Rates

The size of your down payment can significantly impact the mortgage rates you're offered. Larger down payments reduce the loan-to-value ratio (LTV), making the loan less risky for lenders. As a result, borrowers with higher down payments often qualify for lower rates.

For example, a 20% down payment typically eliminates the need for private mortgage insurance (PMI), further reducing overall borrowing costs. However, smaller down payments may still be feasible with certain loan programs, such as FHA or VA loans.

Down Payment Options

- Conventional Loans: Typically require 20% down payment.

- FHA Loans: Allow as low as 3.5% down payment.

- VA Loans: No down payment required for eligible borrowers.

Economic Indicators and Mortgage Rates

Economic indicators provide valuable insights into the direction of mortgage rates. Key indicators include inflation rates, employment data, and housing market trends. For instance, rising inflation often leads to higher mortgage rates as lenders seek to protect themselves against eroding purchasing power.

Similarly, strong employment data and increasing home sales can drive rates higher, reflecting growing demand in the housing market. Conversely, economic slowdowns or declining home sales may result in lower rates as lenders attempt to stimulate borrowing.

Monitoring Economic Indicators

- Inflation Rates

- Employment Data

- Housing Market Trends

Tips for Securing the Best Mortgage Rates Today

Securing the best mortgage rates today requires careful planning and research. Start by improving your credit score, as discussed earlier, and gathering all necessary documentation to streamline the loan application process. Additionally, compare offers from multiple lenders to ensure you're receiving competitive rates.

Consider working with a mortgage broker who can negotiate on your behalf and access a wide network of lenders. Locking in a rate early in the process can also protect you from unexpected rate increases during the application period.

Strategies for Securing Best Rates

- Improve your credit score.

- Shop around for lenders.

- Work with a mortgage broker.

- Lock in your rate early.

Refinancing Options and Mortgage Rates

If you already own a home, refinancing can be an excellent way to take advantage of lower mortgage rates today. Refinancing involves replacing your current mortgage with a new loan at a better rate, potentially reducing your monthly payments and overall borrowing costs.

However, refinancing isn't always the best option. Consider the costs associated with refinancing, such as closing fees and appraisal expenses, and ensure the savings outweigh these expenses. Additionally, evaluate how long you plan to stay in your home, as refinancing may not be worthwhile for short-term homeowners.

Evaluating Refinancing Options

- Compare current rates with your existing mortgage.

- Calculate potential savings and costs.

- Assess your long-term homeownership plans.

Future Predictions for Mortgage Rates

While predicting future mortgage rates is inherently uncertain, experts often provide insights based on current economic trends. As of the latest forecasts, rates are expected to remain relatively stable in the near term, with potential increases if inflation continues to rise.

Homebuyers and homeowners should stay informed about economic developments and consult with financial advisors to make timely decisions. Keeping an eye on Federal Reserve announcements and bond market performance can also provide valuable clues about future rate movements.

Staying Informed About Future Rates

- Follow Federal Reserve announcements.

- Monitor bond market performance.

- Consult financial advisors for personalized advice.

Kesimpulan

Mortgage rates today play a critical role in the homebuying and refinancing processes. By understanding the factors influencing rates, exploring different loan types, and taking steps to improve your financial profile, you can secure the best possible rates for your mortgage. Whether you're a first-time homebuyer or a seasoned property owner, staying informed and proactive is key to achieving your financial goals.

We encourage you to leave your thoughts and questions in the comments section below. Share this article with friends and family who may benefit from the information, and explore other valuable resources on our website to enhance your financial knowledge.